Multiresolution Analysis of Time Series

mra.RdThis function performs a level \(J\) additive decomposition of the input vector or time series using the pyramid algorithm (Mallat 1989).

mra(x, wf = "la8", J = 4, method = "modwt", boundary = "periodic")Arguments

| x | A vector or time series containing the data be to

decomposed. This must be a dyadic length vector (power of 2) for

|

|---|---|

| wf | Name of the wavelet filter to use in the decomposition. By

default this is set to |

| J | Specifies the depth of the decomposition. This must be a number less than or equal to \(\log(\mbox{length}(x),2)\). |

| method | Either |

| boundary | Character string specifying the boundary condition.

If |

Value

Basically, a list with the following components

Wavelet detail vectors.

Wavelet smooth vector.

Name of the wavelet filter used.

How the boundaries were handled.

Details

This code implements a one-dimensional multiresolution analysis introduced by Mallat (1989). Either the DWT or MODWT may be used to compute the multiresolution analysis, which is an additive decomposition of the original time series.

References

Gencay, R., F. Selcuk and B. Whitcher (2001) An Introduction to Wavelets and Other Filtering Methods in Finance and Economics, Academic Press.

Mallat, S. G. (1989) A theory for multiresolution signal decomposition: the wavelet representation, IEEE Transactions on Pattern Analysis and Machine Intelligence, 11, No. 7, 674-693.

Percival, D. B. and A. T. Walden (2000) Wavelet Methods for Time Series Analysis, Cambridge University Press.

See also

Author

B. Whitcher

Examples

## Easy check to see if it works...

x <- rnorm(32)

x.mra <- mra(x)

sum(x - apply(matrix(unlist(x.mra), nrow=32), 1, sum))^2

#> [1] 8.491348e-29

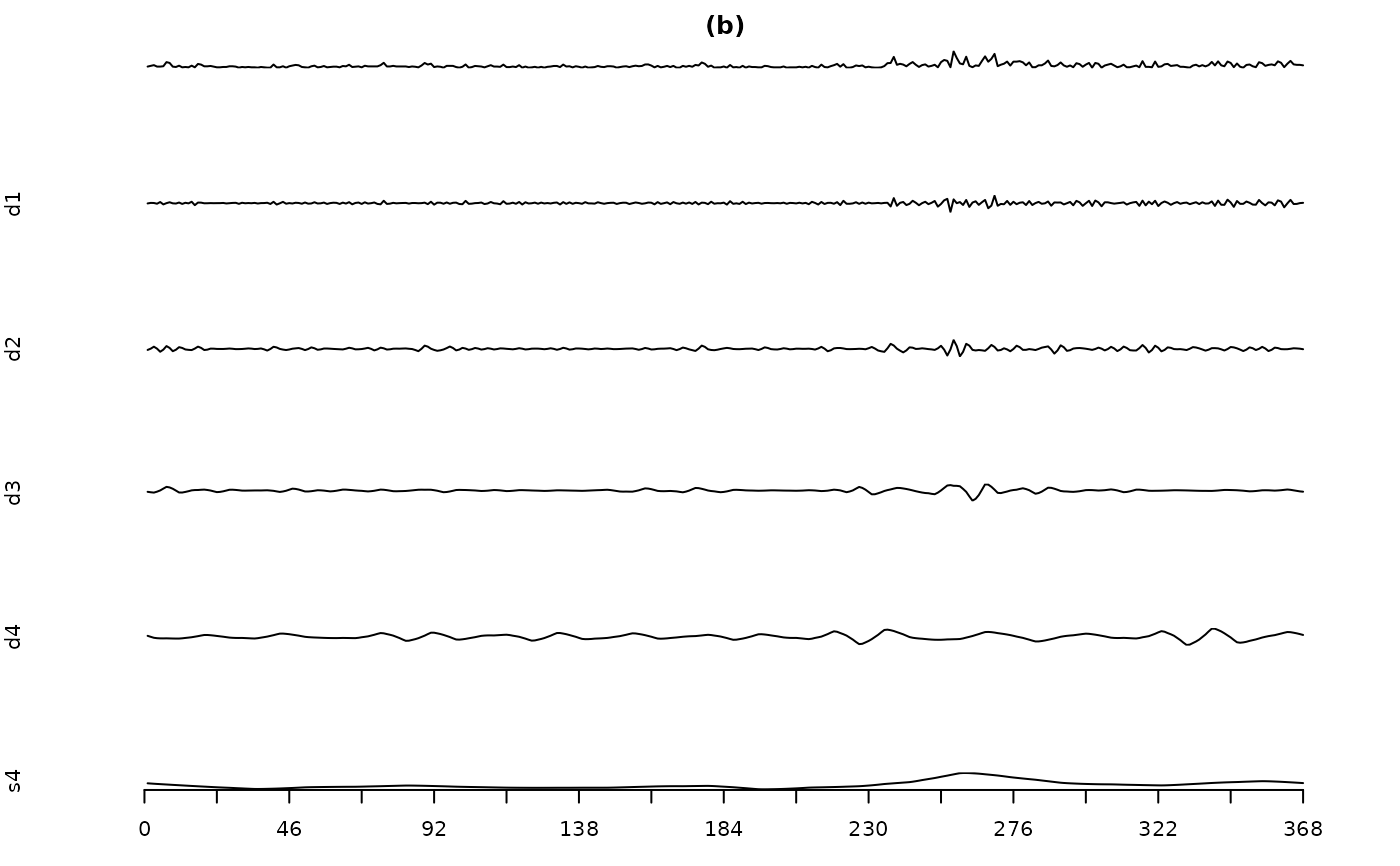

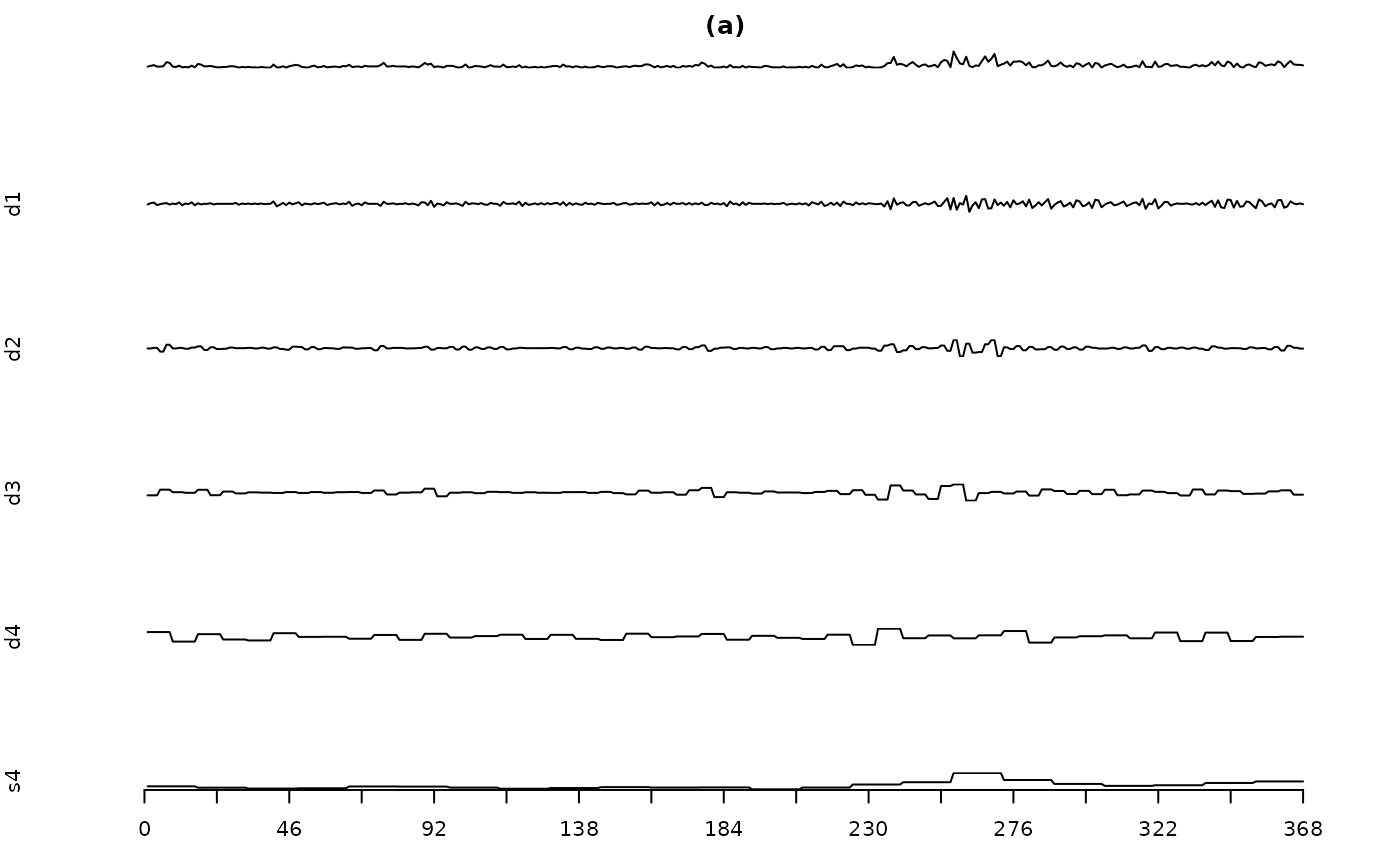

## Figure 4.19 in Gencay, Selcuk and Whitcher (2001)

data(ibm)

ibm.returns <- diff(log(ibm))

ibm.volatility <- abs(ibm.returns)

## Haar

ibmv.haar <- mra(ibm.volatility, "haar", 4, "dwt")

names(ibmv.haar) <- c("d1", "d2", "d3", "d4", "s4")

## LA(8)

ibmv.la8 <- mra(ibm.volatility, "la8", 4, "dwt")

names(ibmv.la8) <- c("d1", "d2", "d3", "d4", "s4")

## plot multiresolution analysis of IBM data

par(mfcol=c(6,1), pty="m", mar=c(5-2,4,4-2,2))

plot.ts(ibm.volatility, axes=FALSE, ylab="", main="(a)")

for(i in 1:5)

plot.ts(ibmv.haar[[i]], axes=FALSE, ylab=names(ibmv.haar)[i])

axis(side=1, at=seq(0,368,by=23),

labels=c(0,"",46,"",92,"",138,"",184,"",230,"",276,"",322,"",368))

par(mfcol=c(6,1), pty="m", mar=c(5-2,4,4-2,2))

plot.ts(ibm.volatility, axes=FALSE, ylab="", main="(b)")

for(i in 1:5)

plot.ts(ibmv.la8[[i]], axes=FALSE, ylab=names(ibmv.la8)[i])

axis(side=1, at=seq(0,368,by=23),

labels=c(0,"",46,"",92,"",138,"",184,"",230,"",276,"",322,"",368))

par(mfcol=c(6,1), pty="m", mar=c(5-2,4,4-2,2))

plot.ts(ibm.volatility, axes=FALSE, ylab="", main="(b)")

for(i in 1:5)

plot.ts(ibmv.la8[[i]], axes=FALSE, ylab=names(ibmv.la8)[i])

axis(side=1, at=seq(0,368,by=23),

labels=c(0,"",46,"",92,"",138,"",184,"",230,"",276,"",322,"",368))