Wavelet Analysis of Univariate/Bivariate Time Series

wave.variance.RdProduces an estimate of the multiscale variance, covariance or correlation along with approximate confidence intervals.

wave.variance(x, type="eta3", p=0.025)

wave.covariance(x, y)

wave.correlation(x, y, N, p=0.975)Arguments

| x | first time series |

|---|---|

| y | second time series |

| type | character string describing confidence interval

calculation; valid methods are |

| p | (one minus the) two-sided p-value for the confidence interval |

| N | length of time series |

Value

Matrix with as many rows as levels in the wavelet transform object. The first column provides the point estimate for the wavelet variance, covariance, or correlation followed by the lower and upper bounds from the confidence interval.

Details

The time-independent wavelet variance is basically the average of the squared wavelet coefficients across each scale. As shown in Percival (1995), the wavelet variance is a scale-by-scale decomposition of the variance for a stationary process, and certain non-stationary processes.

References

Gencay, R., F. Selcuk and B. Whitcher (2001) An Introduction to Wavelets and Other Filtering Methods in Finance and Economics, Academic Press.

Percival, D. B. (1995) Biometrika, 82, No. 3, 619-631.

Percival, D. B. and A. T. Walden (2000) Wavelet Methods for Time Series Analysis, Cambridge University Press.

Whitcher, B., P. Guttorp and D. B. Percival (2000) Wavelet Analysis of Covariance with Application to Atmospheric Time Series, Journal of Geophysical Research, 105, No. D11, 14,941-14,962.

Author

B. Whitcher

Examples

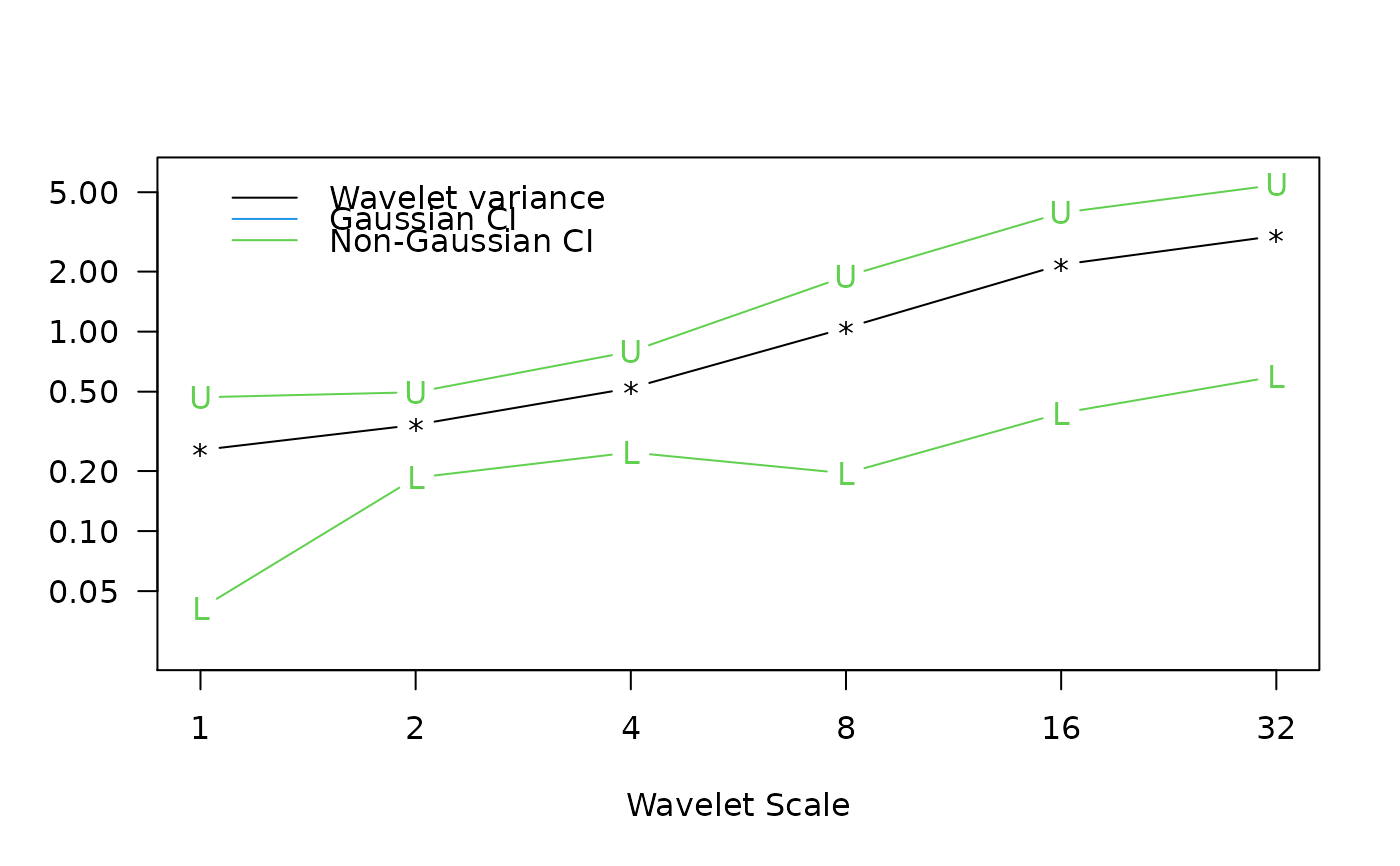

## Figure 7.3 from Gencay, Selcuk and Whitcher (2001)

data(ar1)

ar1.modwt <- modwt(ar1, "haar", 6)

ar1.modwt.bw <- brick.wall(ar1.modwt, "haar")

ar1.modwt.var2 <- wave.variance(ar1.modwt.bw, type="gaussian")

ar1.modwt.var <- wave.variance(ar1.modwt.bw, type="nongaussian")

par(mfrow=c(1,1), las=1, mar=c(5,4,4,2)+.1)

matplot(2^(0:5), ar1.modwt.var2[-7,], type="b", log="xy",

xaxt="n", ylim=c(.025, 6), pch="*LU", lty=1, col=c(1,4,4),

xlab="Wavelet Scale", ylab="")

matlines(2^(0:5), as.matrix(ar1.modwt.var)[-7,2:3], type="b",

pch="LU", lty=1, col=3)

axis(side=1, at=2^(0:5))

legend(1, 6, c("Wavelet variance", "Gaussian CI", "Non-Gaussian CI"),

lty=1, col=c(1,4,3), bty="n")

## Figure 7.8 from Gencay, Selcuk and Whitcher (2001)

data(exchange)

returns <- diff(log(as.matrix(exchange)))

returns <- ts(returns, start=1970, freq=12)

wf <- "d4"

J <- 6

demusd.modwt <- modwt(returns[,"DEM.USD"], wf, J)

demusd.modwt.bw <- brick.wall(demusd.modwt, wf)

jpyusd.modwt <- modwt(returns[,"JPY.USD"], wf, J)

jpyusd.modwt.bw <- brick.wall(jpyusd.modwt, wf)

returns.modwt.cov <- wave.covariance(demusd.modwt.bw, jpyusd.modwt.bw)

par(mfrow=c(1,1), las=0, mar=c(5,4,4,2)+.1)

matplot(2^(0:(J-1)), returns.modwt.cov[-(J+1),], type="b", log="x",

pch="*LU", xaxt="n", lty=1, col=c(1,4,4), xlab="Wavelet Scale",

ylab="Wavelet Covariance")

axis(side=1, at=2^(0:7))

abline(h=0)

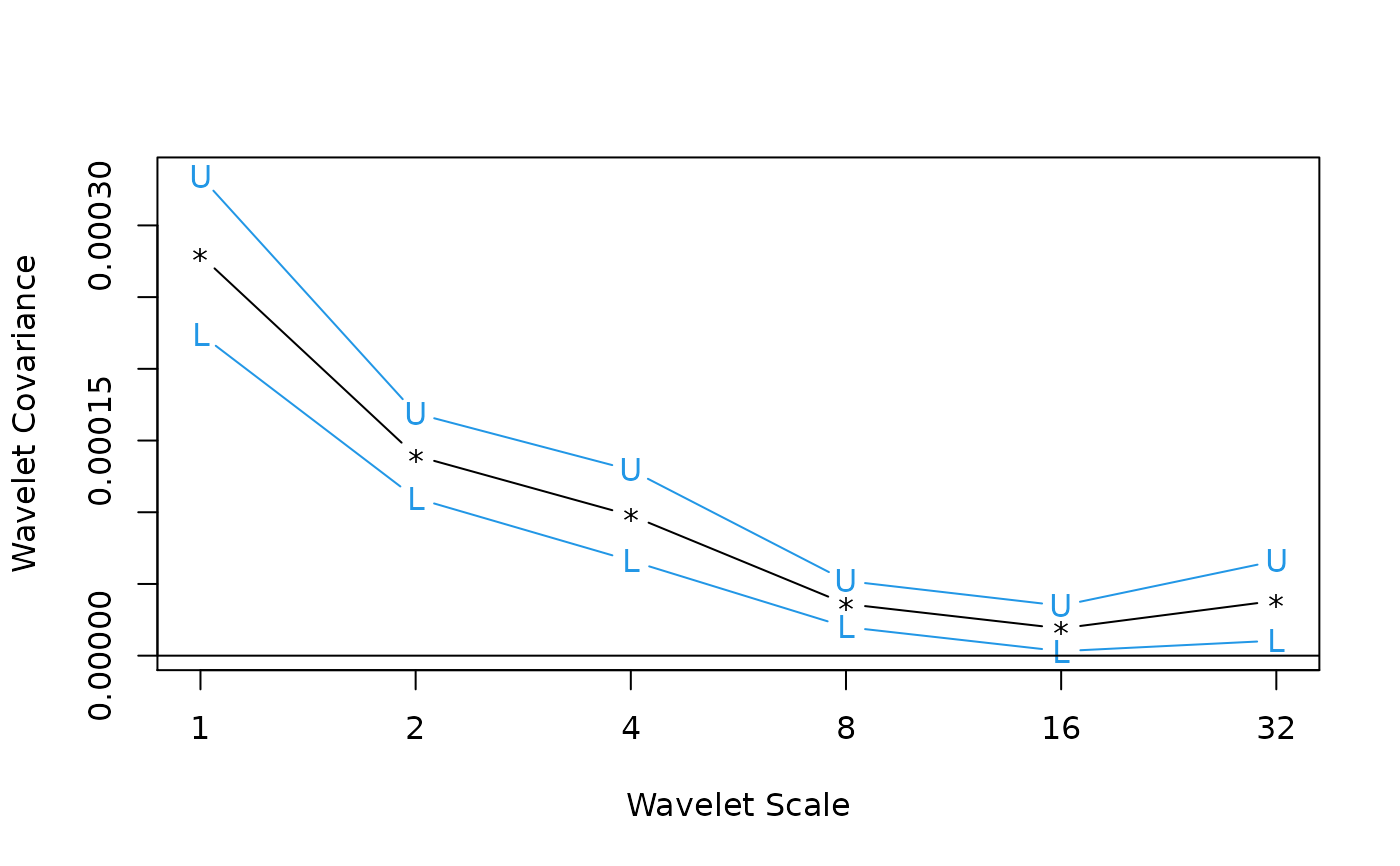

## Figure 7.8 from Gencay, Selcuk and Whitcher (2001)

data(exchange)

returns <- diff(log(as.matrix(exchange)))

returns <- ts(returns, start=1970, freq=12)

wf <- "d4"

J <- 6

demusd.modwt <- modwt(returns[,"DEM.USD"], wf, J)

demusd.modwt.bw <- brick.wall(demusd.modwt, wf)

jpyusd.modwt <- modwt(returns[,"JPY.USD"], wf, J)

jpyusd.modwt.bw <- brick.wall(jpyusd.modwt, wf)

returns.modwt.cov <- wave.covariance(demusd.modwt.bw, jpyusd.modwt.bw)

par(mfrow=c(1,1), las=0, mar=c(5,4,4,2)+.1)

matplot(2^(0:(J-1)), returns.modwt.cov[-(J+1),], type="b", log="x",

pch="*LU", xaxt="n", lty=1, col=c(1,4,4), xlab="Wavelet Scale",

ylab="Wavelet Covariance")

axis(side=1, at=2^(0:7))

abline(h=0)

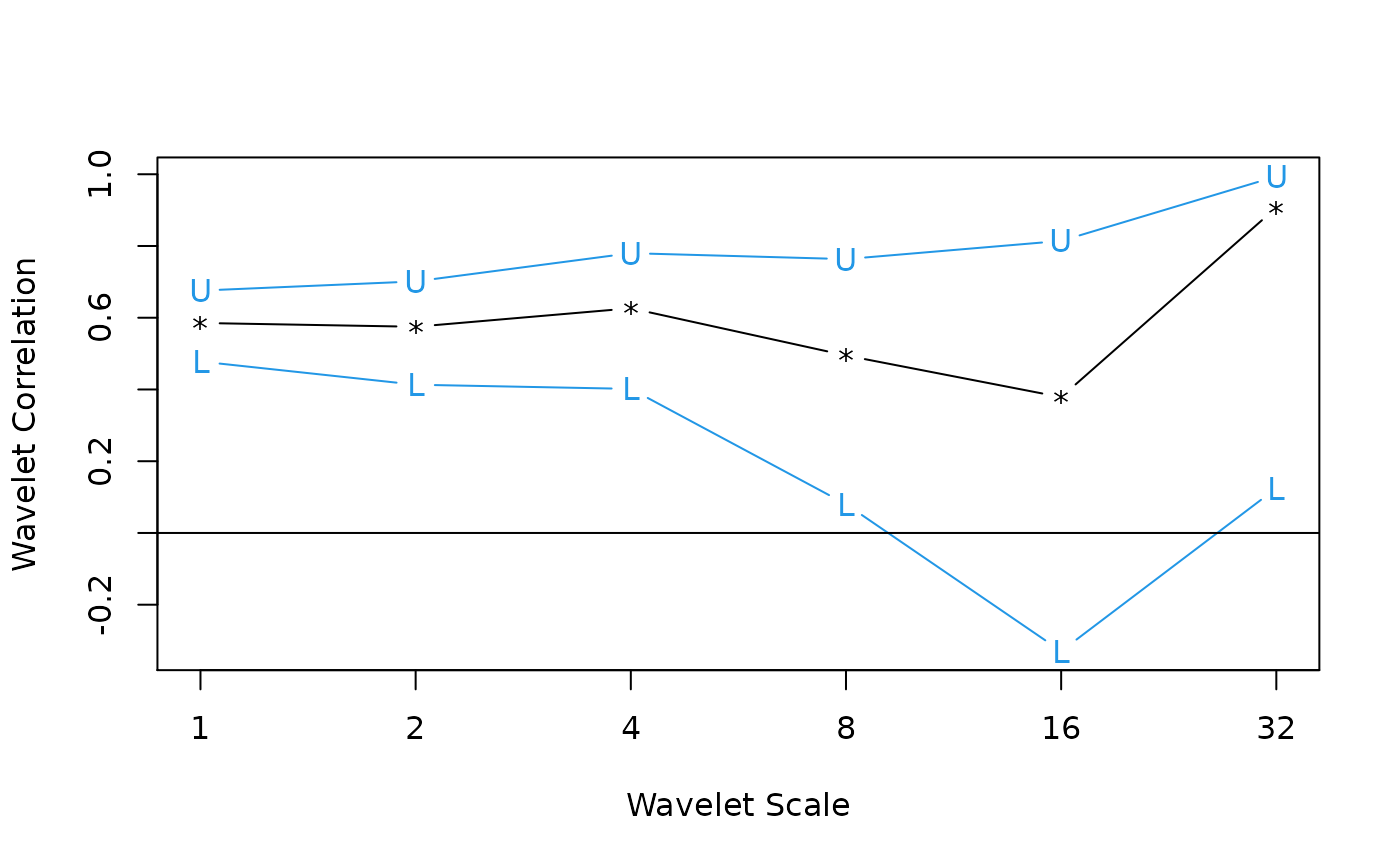

returns.modwt.cor <- wave.correlation(demusd.modwt.bw, jpyusd.modwt.bw,

N = dim(returns)[1])

#> Warning: NaNs produced

#> Warning: NaNs produced

par(mfrow=c(1,1), las=0, mar=c(5,4,4,2)+.1)

matplot(2^(0:(J-1)), returns.modwt.cor[-(J+1),], type="b", log="x",

pch="*LU", xaxt="n", lty=1, col=c(1,4,4), xlab="Wavelet Scale",

ylab="Wavelet Correlation")

axis(side=1, at=2^(0:7))

abline(h=0)

returns.modwt.cor <- wave.correlation(demusd.modwt.bw, jpyusd.modwt.bw,

N = dim(returns)[1])

#> Warning: NaNs produced

#> Warning: NaNs produced

par(mfrow=c(1,1), las=0, mar=c(5,4,4,2)+.1)

matplot(2^(0:(J-1)), returns.modwt.cor[-(J+1),], type="b", log="x",

pch="*LU", xaxt="n", lty=1, col=c(1,4,4), xlab="Wavelet Scale",

ylab="Wavelet Correlation")

axis(side=1, at=2^(0:7))

abline(h=0)