Autocovariance Functions via the Discrete Fourier Transform

my.acf.RdComputes the autocovariance function (ACF) for a time series or the cross-covariance function (CCF) between two time series.

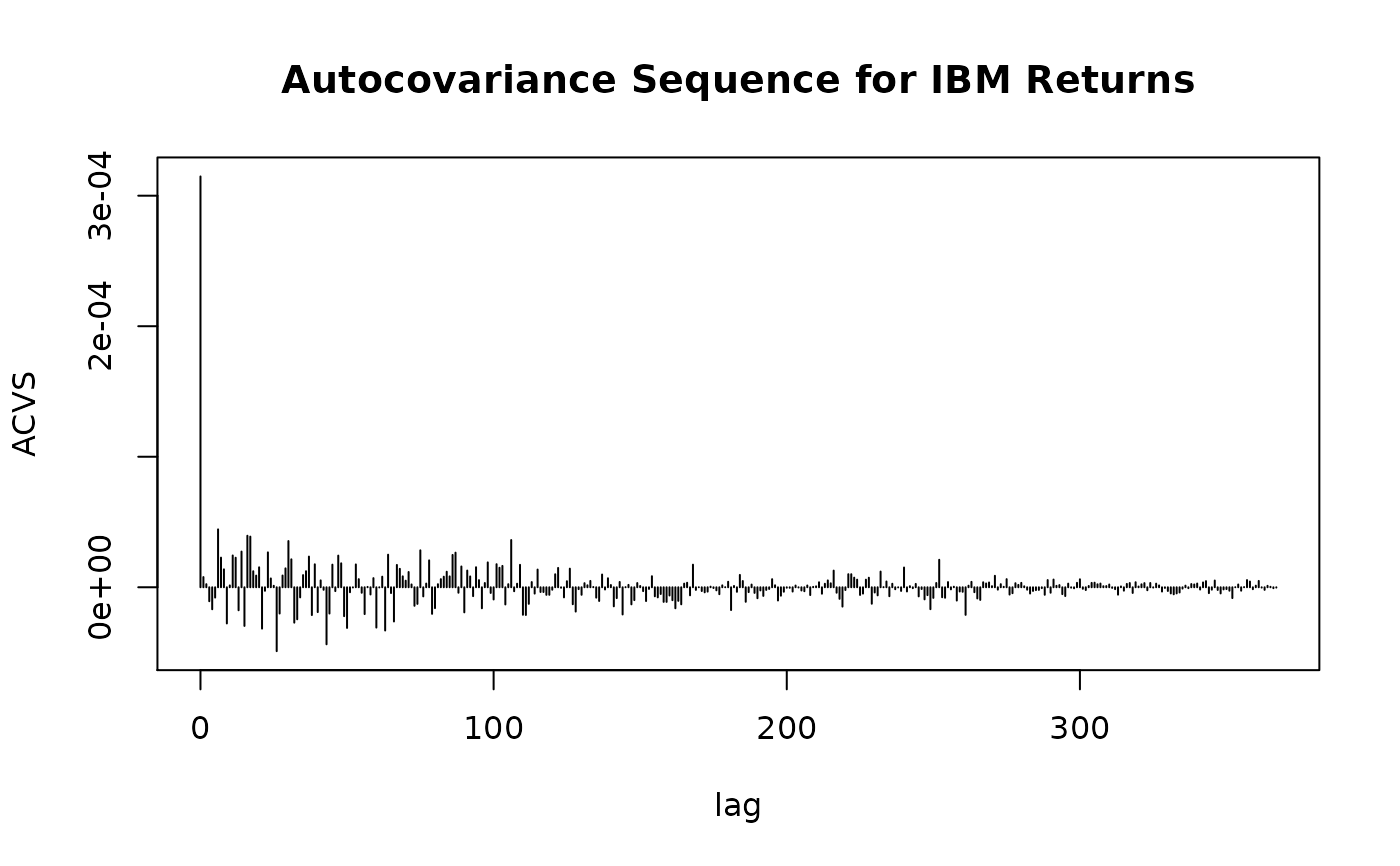

my.acf(x)

my.ccf(a, b)Arguments

| x,a,b | time series |

|---|

Value

The autocovariance function for all nonnegative lags or the cross-covariance function for all lags.

Details

The series is zero padded to twice its length before the discrete Fourier transform is applied. Only the values corresponding to nonnegative lags are provided (for the ACF).

Author

B. Whitcher